Fraud Alert: India Is Losing over ₹22,000 Crore a Year in Cyber Scams — and the Worst Is Yet To Come

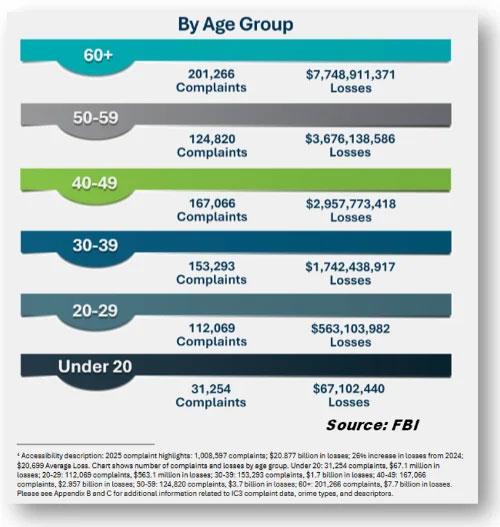

The annual Internet Crime Report for 2025 by the US federal bureau of investigation (FBI) recently made headlines across the world and for good reason. Americans lost nearly US$21bn (billion) to cyber-enabled fraud in a single year, with investment scams (US$8.64bn), cryptocurrency fraud (US$11.36bn) and artificial intelligence (AI)-assisted cons (US$893.34mn—million) among the costliest categories. The numbers from India are no less alarming. In some respects, they are worse.

Quoting data sourced from the Union ministry of home affairs (MHA), a report from The Print says investment scams accounted for more than 75% of the money Indians lost to cybercrimes in 2025. "Indians lost at least ₹22,495 crore to cyber fraud in 2025, as compared to ₹22,845 crore in 2024. But the number of cases went up. A total of 2.81mn (million) cases were reported in 2025, up from 2.26mn in 2024. Despite the rise, the number of first information reports (FIRs) fell to 55,484 in 2025, from 66,370 the year before."

Quoting data sourced from the Union ministry of home affairs (MHA), a report from The Print says investment scams accounted for more than 75% of the money Indians lost to cybercrimes in 2025. "Indians lost at least ₹22,495 crore to cyber fraud in 2025, as compared to ₹22,845 crore in 2024. But the number of cases went up. A total of 2.81mn (million) cases were reported in 2025, up from 2.26mn in 2024. Despite the rise, the number of first information reports (FIRs) fell to 55,484 in 2025, from 66,370 the year before." That translates to roughly US$2.6bn — about one-eighth of American losses. But factor in that Indian incomes are a fraction of American ones, that digital literacy remains patchy, and that legal recourse is far harder to access, and the picture looks considerably bleaker. Over 2.81mn cases were reported last year, up from 2.26mn. With more than 7,700 complaints every single day. India's cybercrime helpline 1930 logged 32.4mn calls in 2025 — which works out to roughly one Indian falling victim to digital or financial fraud every second.

And those are just the reported cases. Most fraud goes unrecorded — victims are embarrassed, sceptical about recovery, or feel the amount isn't worth the trouble of filing a complaint. Of 2.81mn reported cases, only 55,484 FIRs were actually registered, largely because of jurisdictional tangles between state police forces. The more alarming estimate comes from the Indian cybercrime coordination centre (I4C) under the MHA, which projects total cyber fraud losses in 2025 could reach ₹1.2 lakh crore — about 0.7% of India's gross domestic product (GDP). If that number is anywhere near accurate, it would represent roughly five times the officially reported figure, and would make India's cyber fraud problem one of the most severe in the world, relative to the size of its economy.

The Dominant Threat: Fake Investment Platforms

In US, investment fraud accounts for nearly 49% of all scam-related losses. In India, the proportion is even higher — 76% of everything lost to cyber fraud in 2025 went to fake investment schemes: Ponzi traps, counterfeit stock trading platforms, and cryptocurrency scams.

The playbook is grimly familiar by now. Someone contacts you on WhatsApp or Telegram — sometimes as a financial expert, sometimes as a friendly stranger, sometimes impersonating a fund manager at a reputed and well-known brokerage or fund house that you recognise. You get added to a group. Others seem to be making excellent returns. A polished app shows your ‘portfolio’ climbing steadily. You invest small amounts, you see small gains and confidence builds. Then you put in serious money. When you try to withdraw, the platform wants taxes, fees, and margin top-ups. After a while, silence.

A 47-year-old software engineer from Hyderabad's Tellapur area lost over ₹3.2 crore this way. Between December 2025 and January 2026, he transferred ₹3.36 crore into what appeared to be a legitimate stock trading platform he had found through a WhatsApp group. The fraudsters let him withdraw ₹10 lakh early on — enough to convince him the system worked. When he tried to withdraw the rest, withdrawal requests were stonewalled and new demands for ‘service charges’ emerged. By March 2026, the app was gone.

In Mumbai, a 51-year-old share trader from Dadar — someone with years of actual market experience — was cheated of ₹86.9 lakh after being added to a WhatsApp group called ‘F5 Axis Securities Group’. Fraudsters showed him a fake dashboard that made his money appear to grow to ₹2.1 crore. He knew markets. It didn't matter.

In Odisha, the cybercrime branch cracked open a network that had siphoned ₹2.06 crore from a single investor between December 2024 and March 2025, using the same routine: a WhatsApp group, stock tips and promises of professional guidance.

The common thread is always the same — manufactured credibility, engineered urgency and the one promise no honest investment scheme ever makes: guaranteed returns. If anyone is guaranteeing returns, they are running a fraud. Full stop.

Digital Arrest: A Scam India Has Made Its Own

India has spawned a category of fraud with almost no parallel elsewhere — the ‘digital arrest’. Scamsters call posing as officers from the central bureau of investigation (CBI), customs, police, or cybercrime authorities. They tell the victim their Aadhaar card, phone number, or bank account has been linked to drug trafficking, money laundering, or terrorism. The victim is placed under a so-called ‘digital arrest’ — kept on a continuous video call, forbidden from contacting anyone, and threatened with physical arrest the moment they hang up. The coercion can go on for days. Weeks, sometimes and months, in exceptional cases.

Parliament was told in March 2025 that 39,925 such cases were reported as far back as 2022, with losses of ₹91.14 crore that year. By 2024, the number had ballooned to 123,672 cases, with victims of digital arrest collectively losing ₹1,935.51 crore. The victims are not gullible people — they include academics, doctors, bankers, retired bureaucrats and in one documented case, a former senior police officer.

The individual cases are gut-wrenching. SP Oswal, chairman of the Ludhiana-based Vardhman group, transferred ₹7 crore before realising it was a scam. A retired officer from the Indian Air Force (IAF) lost ₹1.59 crore. A retired nursing superintendent was defrauded of ₹83 lakh — money she had saved from her pension. A doctor couple in Delhi lost ₹15 crore to fake legal threats. An 81-year-old retired defence officer in Bengaluru lost ₹1.8 crore.

Then there was the Mangaluru woman who missed a call on 15 January 2025 and called back. The person on the line, posing as an official from Indian Post, told her a parcel she had supposedly sent to China had been intercepted — 150gm of MDMA inside, a prison sentence of 75-plus years. She was told to tell no one and cooperate with the 'investigation.' From 17th January to 4 July 2025, she transferred ₹3.09 crore — in multiple instalments, through RTGS — to accounts the fraudsters controlled. By the time she understood what had happened, the money was gone.

Let this be absolutely clear: there is no such thing as a ‘digital arrest’ in Indian law. Not in any statute, not in any procedure. CBI does not investigate you over WhatsApp. Customs does not put you under video surveillance. Police do not issue digital warrants on Telegram. If someone calls you claiming otherwise, it is 100% fraud. Hang up and call 1930.

The AI Dimension: Cloned Voices, Fake Faces, Manufactured Emergencies

The FBI's 2025 report included AI as a stand-alone section for the first time in its 25-year history, with AI-assisted scams costing Americans nearly US$900mn. India is in the thick of the same shift — arguably faster and more exposed.

A 2025 survey by Observer Research Foundation (ORF) found that 47% of Indian adults have personally been victims of an AI voice-cloning or deepfake scam, or know someone who has — nearly double the global average of 25%. And 83% of Indian victims of AI voice scams suffered actual monetary loss, with almost half losing more than ₹50,000.

The mechanics are disturbingly simple. Fraudsters pull voice samples from social media — a few seconds from a video post or a reel is more than enough for modern AI tools. They call a parent, a spouse, a friend, impersonating someone close to them in a crisis: an accident, an arrest, a medical emergency.

A 68-year-old businessman in Powai, Mumbai, received a WhatsApp call from someone who claimed to be an official at the Indian Embassy in the UAE, saying his son — who works in Dubai — had been arrested. The caller's voice sounded like the son's. It was a clone, scraped from social media videos. The businessman lost ₹80,000 before he realised what had happened.

Deepfakes are increasingly being used in investment fraud, too, with AI-generated videos featuring well-known business figures and celebrities used to push fake schemes. Courts are beginning to take notice — a Delhi court recently granted relief in a deepfake fraud case involving a public figure whose face and voice had been used without consent, calling it a turning point in India's judicial response to AI-enabled financial crime.

The State of Recovery

Three out of four rupees lost to cyber fraud in India are simply not recovered. The national recovery rate improved to 24% in 2025, which is progress, but still means the vast majority of victims never see their money again. Since its launch in 2021, the citizen financial cyber fraud reporting and management system (CFCFRMS), which runs the 1930 helpline, has helped save over ₹7,130 crore across 23 lakh complaints. That is real money saved for real people — but it is still a fraction of what has been lost in that same period.

Speed is the single most important factor. Call 1930 within the first hour of a fraudulent transaction and there is a genuine chance of triggering an account freeze before the money moves. Wait a day, and the odds drop sharply. Cybercriminals disperse stolen funds through dozens of mule accounts within minutes — by the time you have decided whether it is worth reporting, the money is already several layers deep in a chain of accounts, often across state borders.

And increasingly, it is across international borders too. Over 50% of cyber fraud targeting Indians in 2025 is now believed to have originated from scam compounds in Cambodia, Myanmar, and Laos — where trafficked workers are forced to run these operations on an industrial scale (Fraud Alert: Dream Job or Digital Trap? How Lucrative Overseas Offers Are Turning Indians into Bonded Cyber Slaves). Prosecuting those networks from India is, for now, near-impossible.

What You Should Do

1. Call 1930 immediately: Not after you have talked to your family. Not after you have gathered more evidence. Right now, while there is still a chance, the money can be frozen. File a parallel complaint at cybercrime.gov.in. For losses above ₹10 lakh, the system now automatically registers a zero FIR with the e-crime police station in Delhi.

2. Never trust ‘guaranteed returns’: No financial or investment adviser registered with the Securities and Exchange Board of India (SEBI), no legitimate fund, no real brokerage guarantees returns. If someone is promising them, they are lying. Check any investment adviser's registration status on SEBI's public portal before sending a rupee.

3. Official agencies do not work over WhatsApp: CBI, customs, directorate of enforcement (ED), police, Telecom Regulatory Authority of India (TRAI) — none of them will call you on video to conduct an investigation or demand money to settle a case. Any call claiming otherwise is a fraud. Hang up.

4. Verify before you act: If you receive a panicked call from someone claiming to be a family member or friend in trouble, hang up and call them back directly on their known number. AI voice cloning is good enough now to fool even people who know someone well. The callback takes 10 seconds and it will tell you everything you need to know.

5. Screenshot everything: Unified payments interface (UPI) IDs, bank account numbers, contact names, conversation screenshots — preserve all of it. It is the foundation of any recovery attempt or police case.

6. Be careful what you post. Your voice, your face, your daily routine, your family details — all of it is useful to fraudsters. The less you put out publicly on social media, the less they have to work with.

India's digital story is genuinely remarkable. Over 86% of households are connected to the internet, UPI processing billions of transactions every month and financial services are reaching people who have never had a bank account. But the same infrastructure that makes all of this possible is visible to criminals who are better organised, better funded, and faster-moving than most of us realise. This is not a problem that will quietly sort itself out as India gets more digital. If anything, the opposite is happening.

Fraud at this scale is not opportunistic. It is industrial. And it deserves to be treated that way — by regulators, by banks, by law enforcement, and by every one of us who uses a smartphone.

Stay Alert, Stay Safe!

How To Report Cyber Fraud?

Immediately report a cybercrime incident to the National Cyber Crime Reporting Portal http://cybercrime.gov.in or call the toll-free National Helpline number, 1930. To follow on social media: Twitter (@Cyberdost), Facebook (CyberDostI4C), Instagram (cyberdostl4C), Telegram (cyberdosti4c).

Are you a victim of Online Financial Fraud? Immediately call helpline Number 1930 and register your complaint at https://t.co/cr6WZMOi4c pic.twitter.com/HZqUMKSDNF

— Cyber Dost (@Cyberdost) October 12, 2022

If the fraud involves your bank account, you need to immediately email the official email address of your branch (you can find it on the bank's website or in your passbook), with a copy to the bank's customer care. Even if you have called the official customer care number, you must still email a description of your conversation with the bank executive, including the time, date, and duration of the call. This will be helpful if you face a liability issue with the bank.